Understanding Your Payslip

Despite its significance, the importance of a payslip is often overlooked.

A payslip serves as a critical document verifying employment, income, and tax compliance, yet its value extends beyond transactional purposes. It provides transparency into salary breakdowns, deductions, and benefits, empowering employees to manage finances, track expenses, and plan for taxes.

Moreover, payslips are essential for loan applications, credit assessments, and social security benefits. Overlooking payslip accuracy or neglecting to provide detailed information can lead to financial discrepancies, tax issues, and employee dissatisfaction, underscoring the need for precise and timely payslip generation. Your payslip is important for the following reasons:

Employee Rights & Benefit Claims

Serves as evidence of the terms of employment and the deductions made from the employee’s earnings. This is important in ensuring that employees are paid the correct amount and that their rights are protected.

Record of Earnings

This is important for tax purposes, as the employee may need to provide proof of income to government agencies or financial institutions.

Tax Purposes

The payslip contains information to ensure that the correct amount of tax is being paid.

Budgeting

Your payslip indicates the benefits you do not have to acquire for yourself. Eg. Group Life Cover, Funeral Cover etc. You are able to budget accordingly with this information.

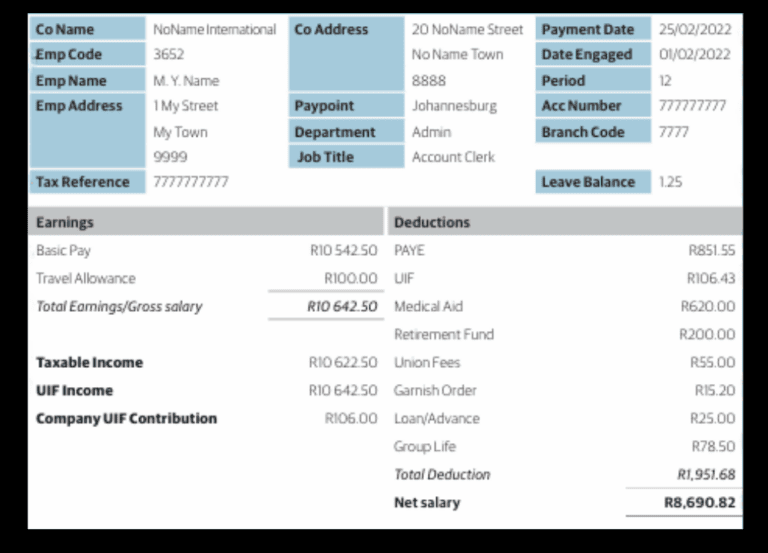

A Typical Payslip includes

Deductions: Income Tax (PAYE - Pay As You Earn), UIF (Unemployment Insurance Fund), Medical Aid, Pension/Retirement Fund, Other Deductions (e.g. Union Fees, Garnishee Orders

Employer Information: Company Name, Company Address, Company Tax Number / VAT Number

Employee Information: Name, Employee Number, TAX / SA ID Number, Job Title, Employee Address, Status: Perm/Temp, Date Engaged with Company, Leave Information & Balances, Payment Information, Pay Date, Pay Period (e.g. monthly/weekly), Gross Pay (total earnings before deductions), Net Pay (take-home pay after deductions), Rate Per Hour, Bank Details of Employer (may include: PAYE & UIF Reference Number, Employee Tax Certificate (IRP5/IT3(a)) details, IRP5: Employer's copy of Tax Certificate submitted to SARS, IT3(a): Employee's copy of the tax certificate for personal tax returns)

Annual Package typically refers to the total yearly compensation or remuneration an employee receives from their employer. This package usually consists of:

Basic Salary: The employee’s monthly salary, paid out 12 times a year.

Annual Bonus: A once-a-year payment, often based on individual or company performance.

Leave Allowance: Paid time off, such as vacation days, sick leave, and family responsibility leave.

Other Allowances: Depending on the company, this might include allowances for things like housing, meals, or entertainment.

Benefits: Contributions to Medical Aid, Retirement Fund (Pension/Provident), Life Insurance, Disability Insurance, Company Specific Benefits

Travel & Cellphone Allowance: A monthly or annual allowance for work-related travel & cellphone expenses

Net Pay

The net salary, also known as the take-home pay, is the amount of money an employee receives after all deductions and taxes have been subtracted from their gross salary. The net salary is calculated by subtracting the following from the gross salary:

Income tax (PAYE – Pay As You Earn)

Unemployment Insurance Fund (UIF) contributions

Skills Development Levy (SDL) contributions

Medical aid contributions (if applicable)

Retirement fund contributions (if applicable)

Other deductions (e.g., life insurance, disability insurance, etc.)

Bonuses

Bonuses are typically calculated as a percentage of an employee’s basic salary or as a fixed amount.

Percentage of basic salary: A percentage of the employee’s basic salary, e.g., 10% or 20%.

Fixed amount: A predetermined fixed amount, e.g., R10,000 or R20,000.

Performance-based: Linked to individual or company performance targets, e.g., meeting sales targets or achieving specific goals.

Discretionary: Awarded at the employer’s discretion, often based on individual performance or contributions.

Guaranteed: A guaranteed bonus, often paid annually, e.g., a 13th cheque.

Some bonuses, like performance-based or discretionary bonuses, may have specific conditions or criteria to meet before payment. Always check the employment contract or company policies for details.

Allowances

Overtime Pay

Overtime is calculated according to the Basic Conditions of Employment Act (BCEA).

Normal working hours: Determine the employee’s regular working hours per week (usually 45 hours).

Overtime threshold: Identify the overtime threshold, which is:

45 hours/week for most employees

50 hours/week for:

- Employees who earn above the threshold (currently R205,433.30 per year)

- Employees who work in certain industries (e.g., agriculture, domestic work)

Overtime hours: Calculate the number of hours worked beyond the threshold.

Overtime rate: Determine the overtime rate, which is:

- 1.5 times the regular hourly rate for the first 10hrs of overtime p/week

- 2 times the regular hourly rate for hours worked beyond 10hrs of overtime p/week

Overtime pay: Calculate the overtime pay by multiplying the overtime hours by the overtime rate

For example, if your monthly basic salary is R20,000, and you receive a 13th cheque (bonus) of R20,000, your gross salary would be: R20,000 (monthly basic) x 12 = R240,000 (annual basic) R20,000 (bonus) = R260,000 (gross salary)

This is the amount used to calculate taxes and other deductions, which are then subtracted to get your net salary (take-home pay).

For example, if your gross salary is R260,000 per year, and the total deductions amount to R80,000 per year, your net salary would be:

R260,000 (gross salary) – R80,000 (deductions) = R180,000 (net salary)

This means your monthly net salary would be: R180,000 ÷ 12 = R15,000 per month before Tax.

Keep in mind that net salary varies depending on individual circumstances, tax brackets, and company-specific deductions.

Example: Regular working hours: 45 hours/week

Overtime hours: 10 hours (beyond the 45-hour threshold)

Regular hourly rate: R50/hour Overtime rate: 1.5 times R50/hour = R75/hour (for the first 10 hours of overtime)

Overtime pay: 10 hours x R75/hour = R750

Note:

Overtime can be paid as cash or taken as time off (with the employee’s consent)

Employees can agree to work overtime in excess of 10 hours per week, but this must be voluntary and in writing

Some collective agreements or employment contracts may have different overtime provisions, so it’s essential to check specific terms and conditions

You can edit text on your website by double clicking on a text box on your website. Alternatively, when you select a text box a settings menu will appear. your website by double clicking on a text box on your website. Alternatively, when you select a text box

Contributions:

1. Employers and employees contribute 1% of the employee’s earnings each (2% total) to UIF.

2. Contributions are deducted from the employee’s salary and paid by the employer to UIF.

Benefits:

1. Unemployment benefits: 38% of average earnings for up to 34 weeks (max. R14,872.50/month).

2. Illness benefits: 38% of average earnings for up to 238 days (max. R14,872.50/month).

3. Maternity benefits: 66% of average earnings for up to 121 days (max. R14,872.50/month).

4. Adoption benefits: 66% of average earnings for up to 10 weeks (max. R14,872.50/month).

Eligibility:

1. Employees who have contributed to UIF for at least 13 weeks.

2. Employees who are unemployed, ill, or on maternity/ adoption leave.

3. Employees who are not receiving a pension or other UIF benefits.

Claims:

1. Employees submit a claim to UIF with required documents (e.g., ID, proof of unemployment).

2. UIF processes the claim and pays benefits directly to the employee.

Note:

– UIF benefits are subject to change, and eligibility criteria may vary.

– Employees can apply for UIF benefits online or at a Labour Centre.

– Employers must register with UIF and submit monthly contribution returns.

1. Employer registration: Employers register with SARS as a PAYE employer.

2. Employee tax registration: Employees provide their income tax reference number to their employer.

3. Gross income calculation: Employer calculates employee’s gross income (basic salary, bonuses, etc.).

4. Tax tables or software: Employer uses SARS tax tables or payroll software to determine the tax amount based on the employee’s tax bracket and gross income.

5. Tax deduction: Employer deducts the calculated tax amount from the employee’s salary.

6. PAYE payment: Employer pays the deducted tax amount to SARS monthly, by the 7th of the following month.

7. IRP5 certificate: Employer issues an IRP5 certificate to the employee at the end of the tax year (February), showing total earnings and tax deducted.

8. Employee tax return: Employee submits their tax return to SARS, using the IRP5 certificate information.

PAYE ensures that income tax is paid regularly, reducing the burden of a large tax bill at the end of the tax year. Employers act as agents for SARS, facilitating tax collection and compliance.

1. Employee contribution: The employee’s portion of the retirement fund contribution is deducted from their salary.

2. Employer contribution: The employer’s portion of the retirement fund contribution (if applicable) is also deducted.

3. Total contribution: The total retirement fund contribution (employee + employer) is reflected on the payslip.

4. Retirement fund: The contributions are paid to the chosen retirement fund.

Payslip reflection:

– Gross income: R20,000

– Employee retirement fund contribution: R2,000 (10% of gross income)

– Employer retirement fund contribution: R1,500 (7.5% of gross income)

– Total retirement fund contribution: R3,500

– Net income (after retirement fund deduction): R16,500

Note:

– Retirement fund contributions are usually tax-deductible for employees.

– Employers may offer a subsidy or contribution towards retirement fund premiums as a benefit.

– Employees can choose to increase or decrease their retirement fund contributions.

– Retirement funds have different plans, benefits, and rules, impacting contributions and payouts

1. Employee contribution: The employee’s portion of the medical aid premium is deducted from their salary.

2. Employer contribution: The employer’s portion of the medical aid premium (if applicable) is also deducted.

3. Total contribution: The total medical aid contribution (employee + employer) is reflected on the payslip.

4. Medical aid scheme: The contributions are paid to the chosen medical aid scheme.

Payslip reflection:

– Gross income: R20,000

– Employee medical aid contribution: R1,500 (7.5% of gross income)

– Employer medical aid contribution: R1,000 (5% of gross income)

– Total medical aid contribution: R2,500

– Net income (after medical aid deduction): R17,500

Note:

– Medical aid contributions are usually tax-deductible for employees.

– Employers may offer a subsidy or contribution towards medical aid premiums as a benefit.

– Employees can choose to upgrade or change their medical aid options, affecting their contributions.

– Medical aid schemes have different plans, premiums, and benefits, impacting contributions and coverage.

1. Union membership: The employee is a member of a trade union.

2. Union fee agreement: The employer and union agree on the union fee amount and deduction process.

3. Deduction: The union fee is deducted from the employee’s salary.

4. Payment to union: The deducted union fee is paid to the trade union.

Payslip reflection:

– Gross income: R20,000 – Union fee deduction: R200 (1% of gross income)

– Net income (after union fee deduction): R19,800

Note:

– Union fees are usually a percentage of gross income (e.g., 1%).

– Employees can choose to join or leave a union, affecting union fee deductions.

– Employers may have agreements with multiple unions, impacting union fee deductions.

– Union fees fund union activities, negotiations, and member benefits.

Types of union fees:

– Monthly subscription fees

– Levy fees (for specific union activities or events)

– Special resolution fees (for extraordinary union expenses)

Union benefits:

– Collective bargaining and negotiations

– Representation and support

– Training and development

– Industrial action and dispute resolution

A garnish order is a court order that is served by the sheriff of the court on the employer ordering the employer to make deductions from an employees salary or wage in settlement of a debt owed by the employee to a third party creditor.

Contributions:

1. Employers with a payroll of over R500,000 per annum must pay 1% of their total payroll to SDL.

2. The levy is calculated monthly and paid to SARS (South African Revenue Service).

Purpose:

1. Fund skills development programs and training initiatives.

2. Support the National Skills Development Strategy.

3. Encourage employers to invest in employee training and development.

Exemptions:

1. Employers with a payroll under R500,000 per annum.

2. Public service employers (government departments).

3. Certain non-profit organizations (e.g., charities, NGOs).

Benefits:

1. Employers can claim back a portion of their SDL contributions by:

– Implementing approved skills development programs. – Submitting a Workplace Skills Plan (WSP) and Annual Training Report (ATR).

– Participating in Sector Education and Training Authorities (SETAs).

2. SDL funding supports various training initiatives, such as:

– Apprenticeships

– Learnerships

– Bursaries

– Skills programs

Administration:

1. SARS collects SDL contributions.

2. The National Skills Authority (NSA) oversees SDL distribution.

3. SETAs manage skills development programs and funding allocation.

By investing in skills development, employers can enhance their workforce’s capabilities, increase productivity, and contribute to South Africa’s economic growth.

1. Employer contribution: The employer pays a premium for the group benefit.

2. Employee contribution: The employee may also contribute to the premium through salary deductions.

3. Benefit amount: The benefit amount is determined by the group scheme and employer.

4. Payslip reflection: The employee’s contribution (if applicable) is deducted from their salary and reflected on the payslip.

Payslip example:

– Gross income: R20,000 Employer issues an IRP5 certificate to the employee at the end of the tax year (February), showing total earnings and tax deducted.

– Group life insurance deduction: R50 (employee contribution) Employee submits their tax return to SARS, using the IRP5 certificate information.

– Group disability insurance deduction: R75 (employee contribution)

– Net income (after deductions): R19,875

Note:

– Group benefits provide employees with financial protection and peace of mind.

– Employers can choose to offer various group benefits to attract and retain employees.

– Group benefits may have tax implications for employees and employers.

– Employees should review their group benefits regularly to ensure adequate coverage.

What no-one tells you about your first payslip | Standard Bank

You’ll have certain expectations about earning your first salary; in fact, you probably already know how you’re going to spend it, but many new employees are surprised when the amount that hits their bank account differs from their salary. That’s thanks to all the deductions and new financial responsibilities and considerations you’re dealing with.

Basic Guide to Payslips | Department of Employment & Labour

Understanding Your Pay Slip: A Guide for Employees